Brought to you by Primer – Primer unlocks B2C ad channels for B2B marketers with precision targeting and next-gen measurement

There are two ways you’re wasting ad budget: (a) you pay to reach people who will never buy, and (b) the buyers who do show up walk away unidentified. Primer fixes both. This includes excluding the wrong people across Meta and Google before you pay for the impression. No more burning budget on students, competitors, and tire-kickers.

You get unlimited website reveals: every account researching you, identified – no caps, no per-reveal pricing. See who’s actually in-market and feed it straight back into targeting.

GTMnow Network exclusive offer: Extended 45 day trial and 15% off with code GTM15 – just apply the code when you go to upgrade from the free trial.

See who’s really in your funnel: sayprimer.com

How AI-Native Companies Are Scaling on a Direct Enterprise Sales Motion

The PLG story has owned the AI growth narrative for two years, and it deserved to. But the companies quietly posting the same numbers (or more) are doing the opposite.

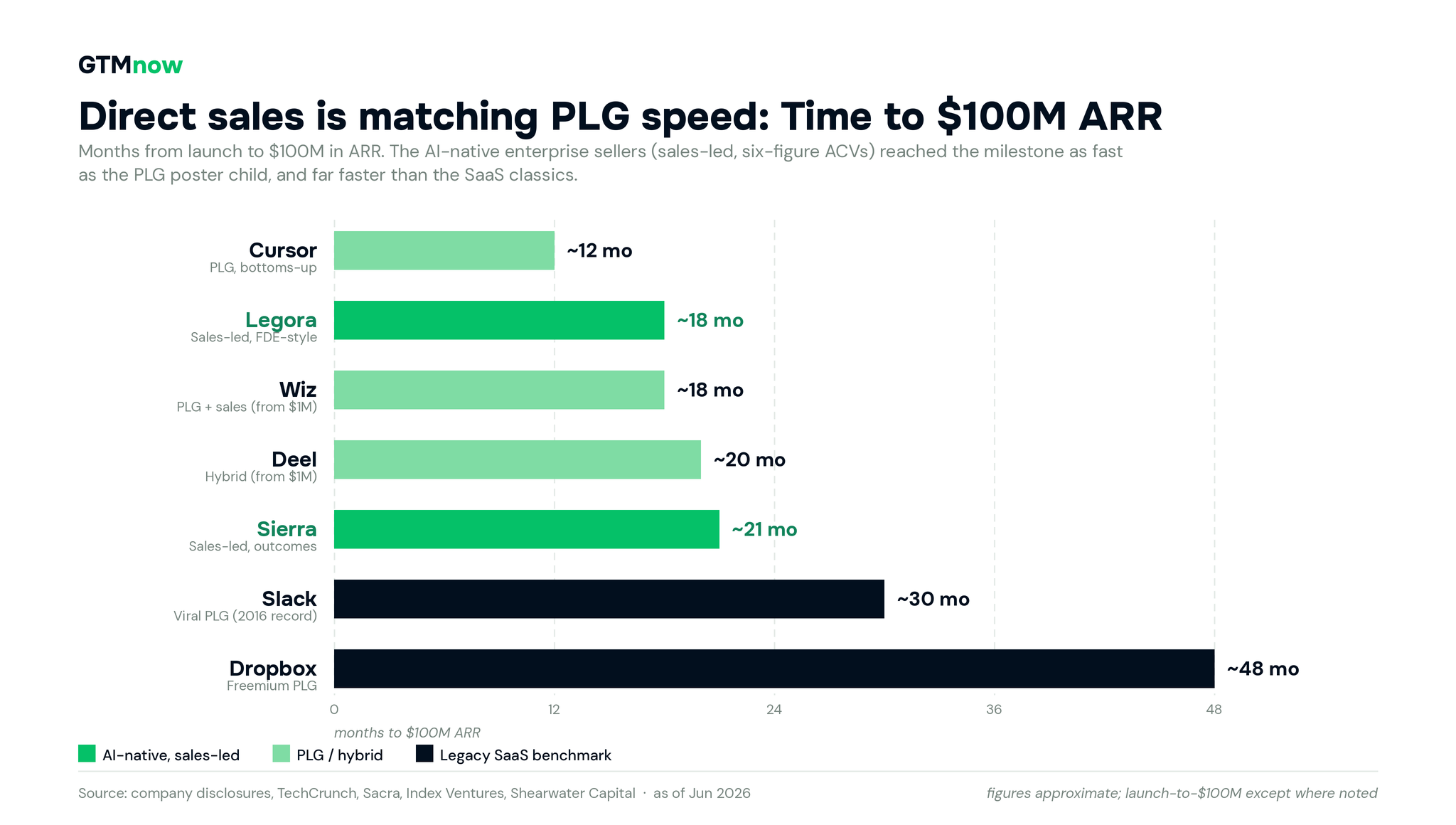

Legora went from $1M to $100M in ARR in about 18 months, selling to the most procurement-heavy buyers on earth, global law firms like White & Case and Linklaters.

Sierra hit a $100M ARR run rate in 21 months and now works with 40% of the Fortune 50, with year-one contracts running into the hundreds of thousands.

Decagon tripled revenue year over year to roughly $35M by October 2025, adding more than 100 enterprise logos across airlines, banks, and telecom.

None of these is a self-serve product you can sign up for at your leisure. Every company has a sales rep in every deal, a six-figure ACV, and a buyer who didn’t get full product access before a contract existed. They are growing at PLG speed on a sales-led motion.

Here is how they’re doing it and how you can too.

The fast risers aren’t all product-led

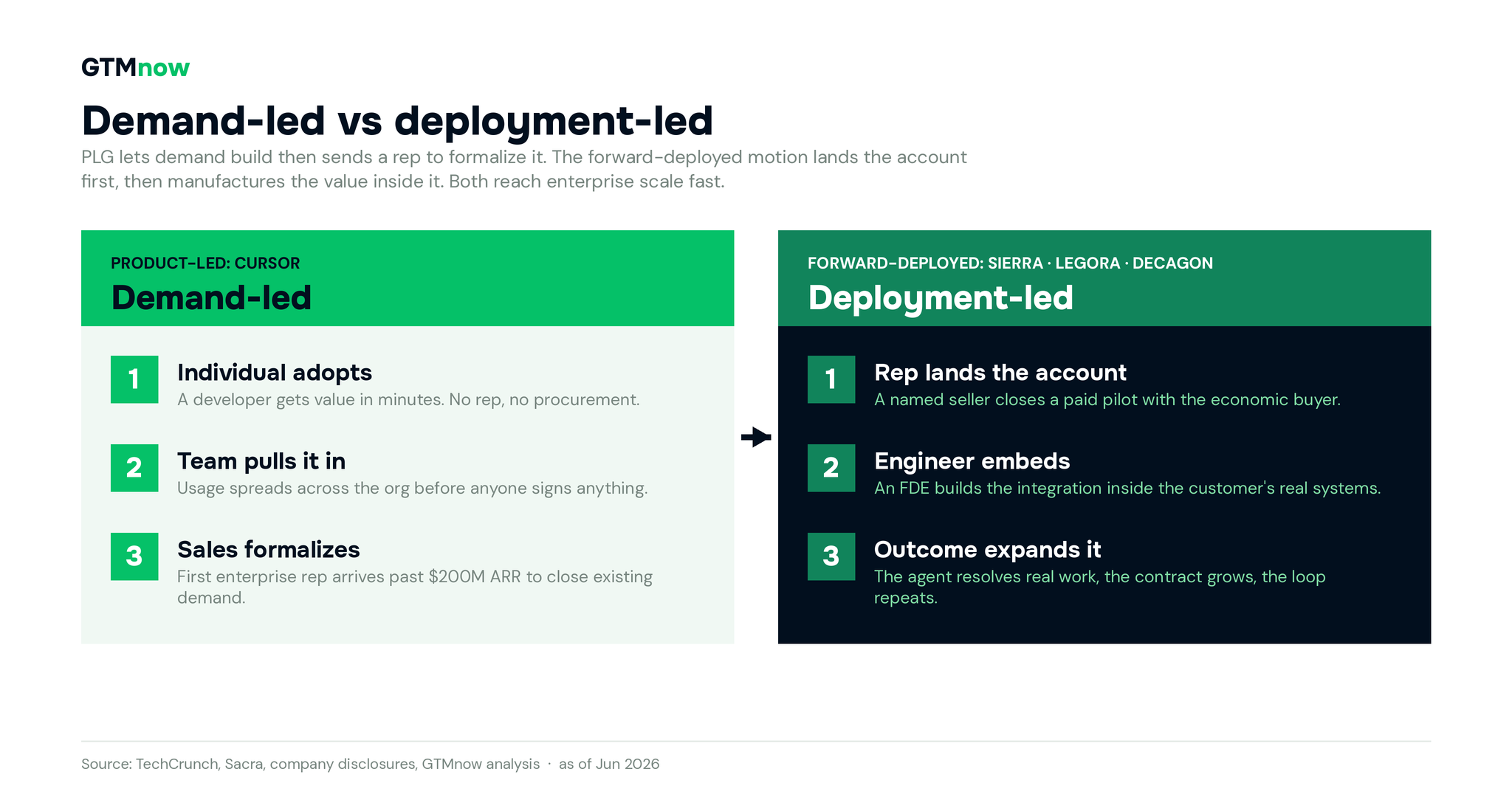

The default explanation for AI’s growth records is bottom-up adoption. Cursor earned that reputation, reaching $100M ARR in twelve months and $2B+ by February 2026 with zero outbound sales until late 2025, simply because developers couldn’t stop pulling it into their companies. Enterprise revenue climbed from roughly 25% of the mix to nearly 60% as the first reps arrived past $200M ARR to formalize demand that already existed.

That motion works when one person can adopt the product alone and get value in minutes. It breaks the moment the buyer is a general counsel, a head of CX, or a CIO who will never personally try the tool, and whose company needs the thing wired into a CRM, a billing system, and a compliance review before it does anything useful.

So a different set of companies skipped the PLG flywheel entirely.

They sell directly to the economic buyer, and they grow just as fast. The speed is coming from a sales motion built specifically for AI.

The two AI-native sales-led companies reached $100M ARR as fast as the PLG record holder.

The motion: sales lands it, an engineer makes it real

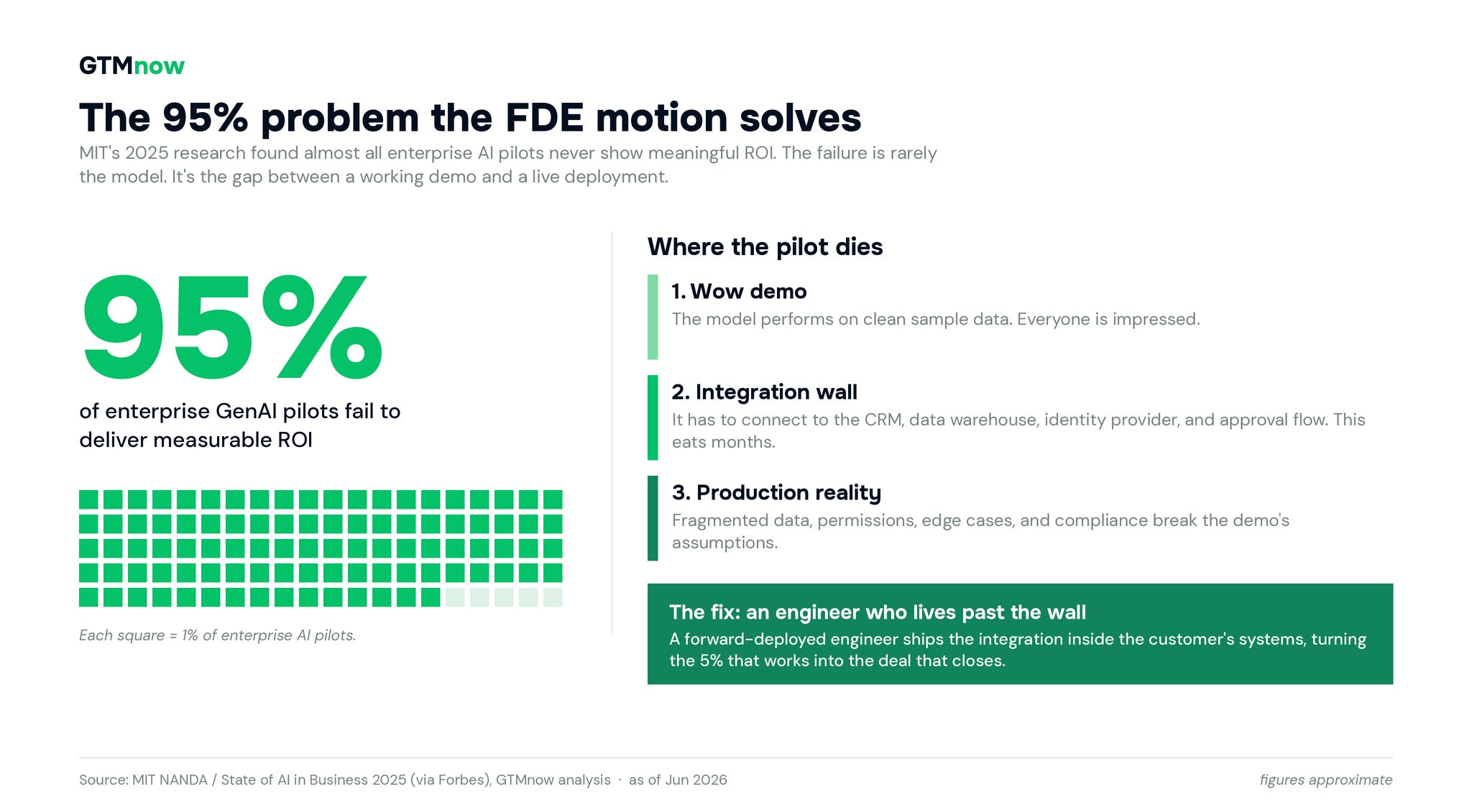

The traditional enterprise playbook is linear: build the product, hand it to sales, sales closes, customer success onboards, and the customer figures it out. That works for a CRM with a known job to be done. It collapses for AI because the gap between a great demo and a working deployment is where most AI pilots crumble. MIT’s 2025 research put the failure rate of enterprise AI pilots at 95%, and most of the failure was implementation, not the model.

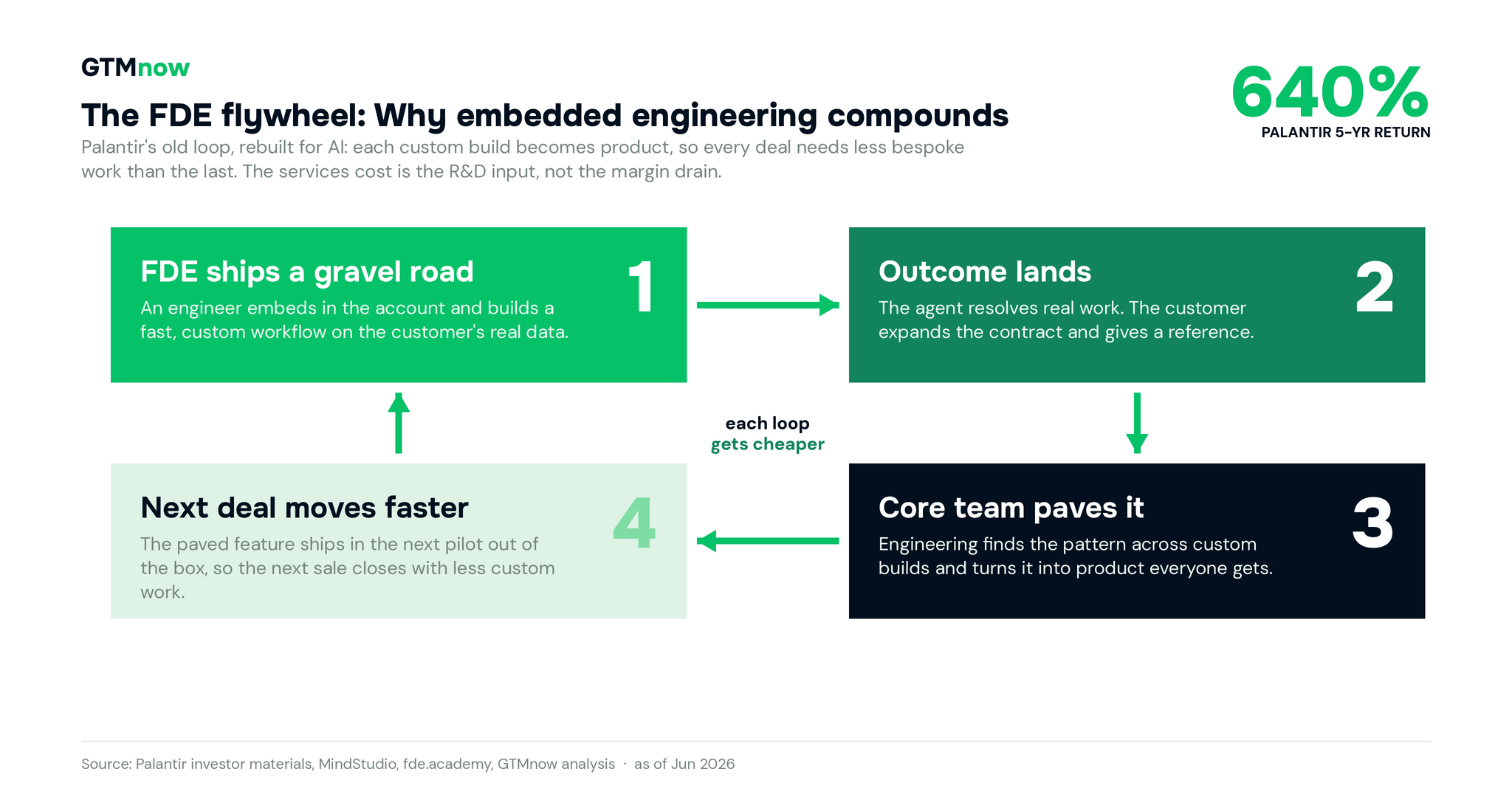

The companies winning closed that gap by moving an engineer into the room. The role has a name now, the forward-deployed engineer, and it was Palantir’s invention from the early 2010s, when its intelligence agency customers couldn’t even describe what they needed. Palantir’s answer was to embed engineers inside the customer to build in real time. That model was mocked for a decade as expensive consulting wearing a software costume, right up until the stock returned roughly 640% over five years.

Almost every enterprise AI pilot dies at the integration wall. The FDE is who gets it past.

What a Forward Deployed Engineer (FDE) is

An FDE is a senior engineer who embeds with the customer for the length of a deployment, writes production code in the customer’s environment, runs technical discovery, and ships the integration that makes the agent work. It is not a renamed solutions engineer. A solutions engineer sells the product and hands it off pre-contract. An FDE, on the other hand, ships the product into production post-contract. One closes the demo, the other closes the gap between the demo and live.

This is now the standard org pattern, not a fringe experiment. Decagon assigns dedicated Agent Product Managers and forward-deployed engineers who embed with each enterprise customer, taking deployments from discovery to live in roughly six weeks. The frontier labs run the same play: Anthropic’s $1.5B Deloitte joint venture and OpenAI’s $10B Bain alliance are, underneath the framing, FDE staffing pacts. When the model makers themselves decide deployment needs embedded engineers, it’s a good sign for application-layer startups building on top of them should take the hint.

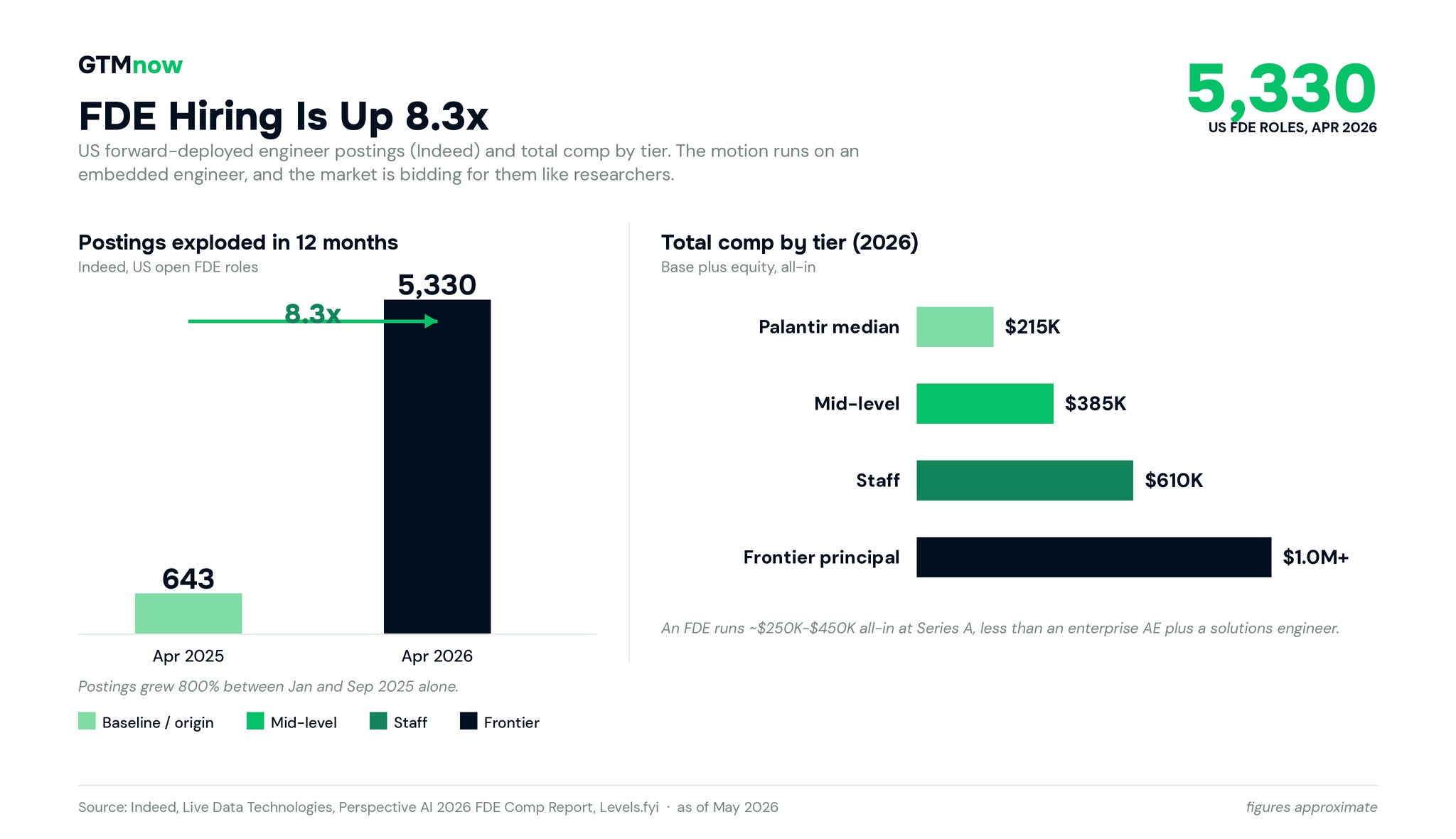

The embedded engineer is the load-bearing hire, and the market is paying for it.

PLG lets demand build, then formalizes it. The FDE motion manufactures demand inside the account.

Why the FDE motion compounds instead of just costing more

The obvious objection is the margin. Embedding engineers in every account sounds like a services business with a software logo, and for fifteen years, that was the consensus read on Palantir. The reason it isn’t a consulting trap is a feedback loop, Palantir named it the gravel road to paved highway.

An FDE builds a fast, custom workflow for one customer, a gravel road. The core engineering team then studies the gravel roads across many customers, finds the repeated pattern, and turns it into a product – a paved highway every future customer gets out of the box. Each custom build makes the next deployment cheaper, so the motion gets more efficient at scale rather than less. So the services’ work isn’t the cost of the model, it’s the R&D input that feeds it.

Decagon productized this directly. Its Agent Operating Procedures let CX teams define workflows in natural language that compile into code, which is exactly the gravel-road work an FDE used to do by hand, paved into a feature customers run themselves. Sierra did the same with Ghostwriter, an agent that builds agents from a customer’s SOPs and recordings, explicitly built to reduce the on-site engineering each new deployment needs. The custom work of the early deals becomes the product surface of the later ones.

The economics back it up. A forward-deployed engineer runs approximately $250K to $450K all-in at Series A, which is less than the fully loaded cost of an enterprise AE plus a solutions engineer, and the FDE produces compounding growth. The compounding curve and the sales-only curve diverge around month six.

The loop that turns embedded fieldwork into a product that closes the next deal faster.

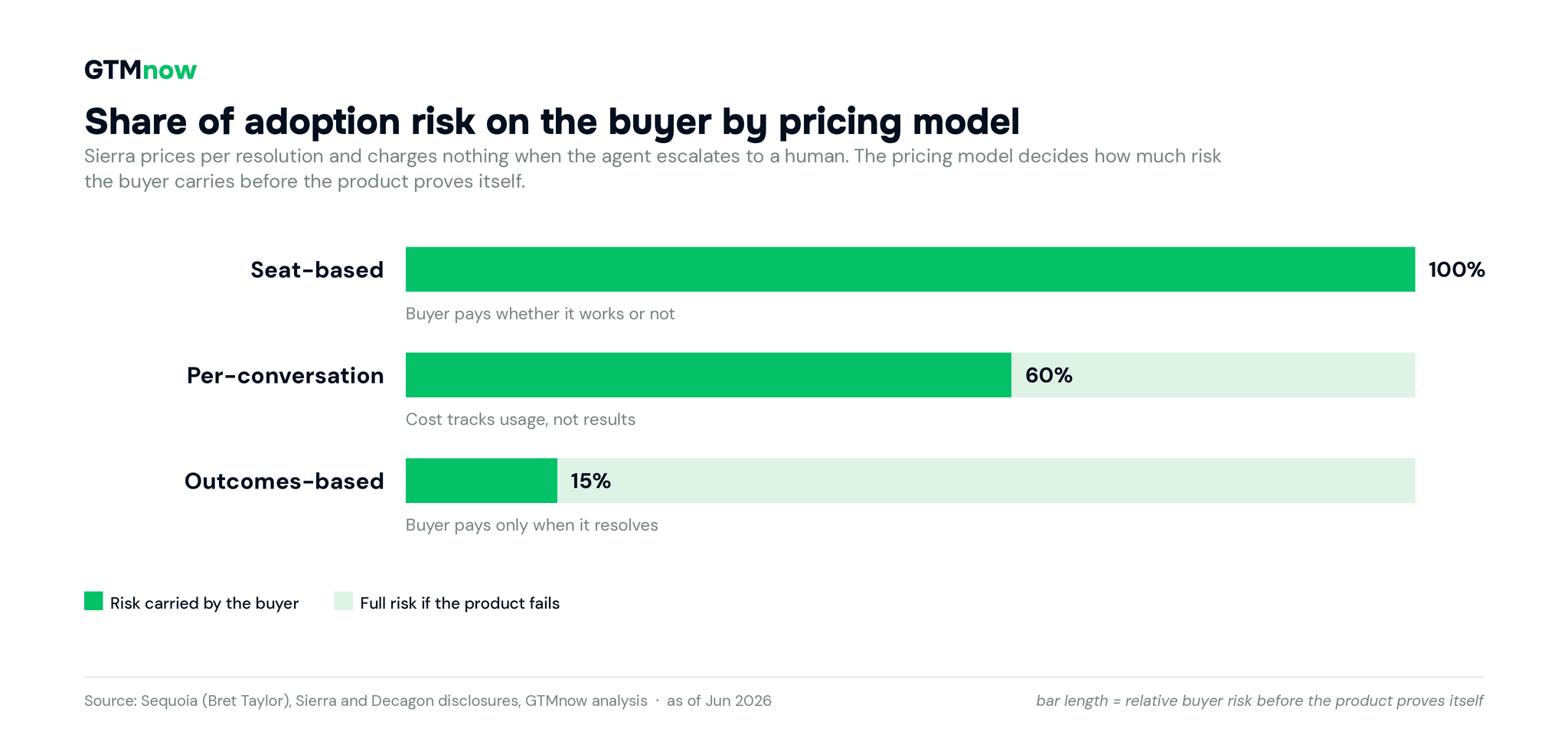

Pricing is doing the selling

A direct AI sale has one objection above all others: will this actually work on our data, or are we paying six figures for a demo that doesn’t survive contact with reality? The fastest companies answer it with the contract itself.

Sierra prices on outcomes. As founder Bret Taylor, the former Salesforce co-CEO now running Sierra, describes it: the customer pays a pre-negotiated rate when the AI agent resolves an issue autonomously and pays nothing when it escalates to a human. He frames it as the natural next step in software’s evolution, from perpetual licenses to subscriptions to paying for a job well done.

Decagon offers per-conversation and per-resolution pricing on the same logic. The effect is the same in both cases: the vendor only makes money when the product works, so the buyer’s risk drops and the deal moves.

Pricing on outcomes shifts adoption risk off the buyer, and it has built a $15.8B company.

PLG made software sell itself, and that story isn’t wrong. But it influenced a perception that a direct sales motion was the slow, old way to grow. Legora, Sierra, and Decagon are the counterexamples. Built right, direct enterprise sales move as fast as any flywheel.

Tag @GTMnow so we can see your takeaways and help amplify them.

SpaceX formally agreed to acquire Cursor for $60 billion in stock, days after its record Nasdaq IPO.

Snap unveiled SPECS, their new augmented reality glasses. Fully standalone, 132 grams, 51-degree field of view and available for pre-order at $2,195 this fall. Then Meta said it’s launching a new line of smart glasses, dubbed Meta Glasses, starting at $299.

VC: “We Don’t Fund Good Companies” : A $1.5B VC Explains Why | Ben Lerer, Lerer Hippeau

GTM: How to Use Sales Comp as a GTM Lever | Siva Rajamani (Everstage CEO)

GTM: How to Win at Paid Advertising in the AI Era | Keith Putnam-Delaney, Primer CEO

VC: How Benchmark Invests & What to Know on GTM | Chetan Puttagunta (GP)

Listen through the links in the page above or by searching wherever you get your podcasts “The GTMnow Podcast.”

Prometheus – raised $12B at a $41B valuation. This is Jeff Bezos’s physical AI startup building software to automate the design and manufacturing of complex physical systems, from jet engines to drug compounds.

Newton – launched mainnet beta – an onchain authorization layer that stops transactions before they settle if they break policy. Crypto solved settlement and skipped authorization. Newton is building that missing layer.

Mutiny – launched an AI agent that takes accounts from cold to closed – one platform replacing ABM, sales enablement, and AI sales tools. Connects to your CRM, calls, and email to automate the buyer experiences that actually win deals. 3,000 companies including Rippling, Snowflake, and Uber are already on it.

Attention – raised $30M Series B led by RTP Global. They are the AI platform that acts on sales calls, not just records them. Most tools tell you what happened. Attention drafts the follow-up, updates the CRM, and runs the next play.

Redo – raised $81M at a $1.25B valuation led by Smash Capital, Pelion Venture Partners, and Cervin Ventures. To celebrate, they’re giving shoppers $100 to spend at Redo brands instead of running a traditional announcement.

Runlayer – raised $30M from Felicis and Khosla Ventures to help companies say yes to agents without losing control. Identity-aware permissions, full observability, runtime security – one platform. Customers include Instacart, Gusto, Decagon, and dbt Labs.

Coval – raised $28M Series A led by Norwest VP to build the simulation and evaluation platform for voice and chat agents. The same approach that made autonomous vehicles trustworthy can do the same for conversational AI.

Scaled Cognition – raised $100M Series A led by Khosla Ventures – AI models built to tell the truth, not just sound confident. Enterprise hallucination rates are 5x what companies think. They rebuilt the architecture from first principles so reliability is engineered in, not bolted on.

General Intuition – raised $320M at a $2.3B valuation led by Khosla Ventures to build AI agents that generalize from gameplay to the real world. Billions of action-labeled gameplay clips from 17M users – not just video, but the exact buttons pressed and when. The same model playing Fortnite is powering their quadruped robot.

Airwallex – raised $320M at an $11B valuation led by Addition to build the intelligent layer on global financial rails. Two new products: T:0, an AI-native finance platform, and Airi, an agentic wallet for when software agents transact on your behalf.

-

Account Executive, SMB at Closinglock (Austin, TX)

-

Enterprise Account Executive, APAC (Sydney, Australia)

-

Account Executive, SLED Government at Vanta (Remote – US)

-

Broker Partner Manager (Broker Development Representative) at TrustLayer (Hybrid – Tampa / St. Pete, FL)

-

Solutions Engineer (Pre-Sales) at Noibu (Hybrid – Ottawa, Ontario)

See more top GTM jobs on the GTMfund Job Board.

Upcoming events you won’t want to miss:

-

Lenny & Friends Summit: September 10, 2026 (San Francisco, CA)

-

Dreamforce 2026: September 15–17, 2026 (San Francisco, CA)

-

INBOUND: September 16–18, 2026 (Boston, MA)

-

Pavilion GTM2026: September 28–October 1, 2026 (NYC, NY)

-

Moment 2026: October 6, 2026 (NYC, NY)

-

CVC Week by Counterpart Ventures: September 29, 2026 (San Francisco, CA)

-

Customer Success Week: October 5-9, 2026 (NYC, NY)

-

TechCrunch DISRUPT: October 13–15, 2026 (San Francisco, CA)

Some GTMnow Network love to close it out – we appreciate you.