This is Part IV of the Deconstructing GTM series. If you missed the previous editions, you can catch up on them here: Read Part I (ClickUp), Part II (Vanta at $100M), and Part III (Gamma at $100M).

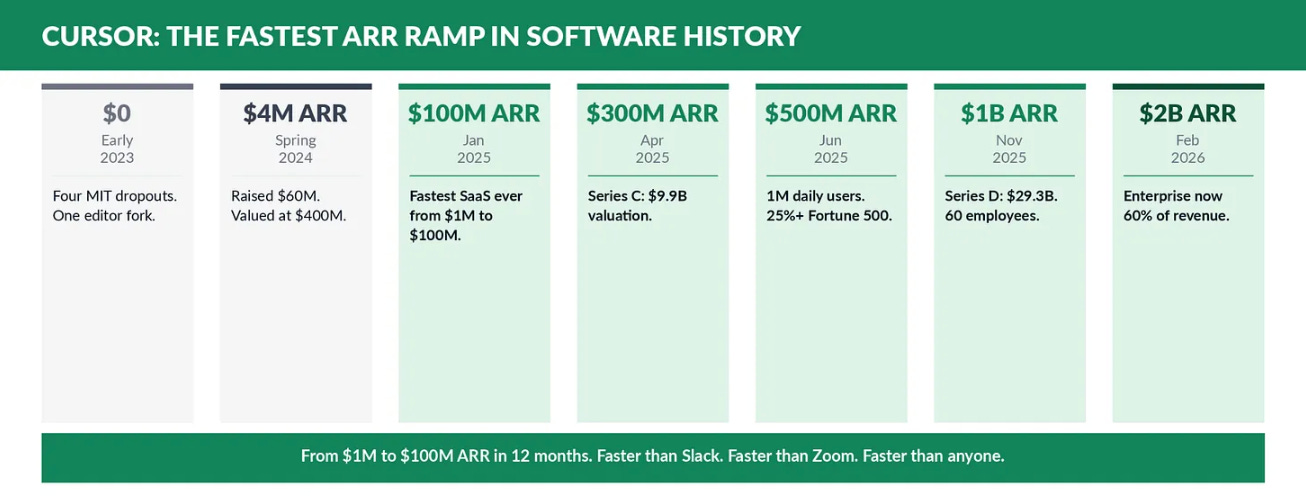

Slack took two and a half years to reach $100M ARR. Dropbox took four years. Cursor took twelve months. From $1M to $100M ARR faster than any software company in history. Then it doubled to $300M in three more months. Then $500M three months after that. Then $1B by November 2025, and then $2B by February 2026.

Cursor was founded by four MIT students. They used no marketing budget initially, zero outbound sales until late 2025, but had a product their users couldn’t stop talking about.

Here’s what you’ll learn from this edition:

- Why forking VS Code instead of building a plugin was the biggest GTM decision Cursor ever made

- The metric that predicted success, and why it wasn’t DAUs or signups

- How Cursor spent zero dollars on marketing to reach $100M ARR

- The enterprise motion built on developer smuggling, not enterprise sales

- Why they built their own AI models after swearing they never would

- The one thing Truell says will survive AI taking over most of software development

- The SpaceX deal, the $60B valuation, and what it tells you about where the market is going

Sales today still relies on manual work: stitching together “Frankenstacks” and toggling between a dozen tabs just to log a single call.

Reevo is breaking the mold. As a vertically integrated Revenue Operating System, Reevo replaces the fragmented maze with a single, AI-native workspace. It captures 100% of your first-party data, from emails to meeting recordings, to help reps find high-intent buyers, automate administrative “garbage,” and generate context-rich outreach that actually sounds human.

No more wasting time on data entry or disconnected tools. It’s one unified engine for the entire revenue cycle. Go Stackless. Learn more at reevo.ai.

Act 1: The false start and the real bet

$0 to $4M ARR (2022 to early 2024)

Before the growth curve, there was a wrong turn nobody remembers. Cursor buried it fast.

In 2021, while still at MIT, the four co-founders were obsessed with AI. They’d seen GitHub Copilot launch. They’d felt what it meant for the first time to have AI genuinely inside a professional workflow. So they decided to start a company.

Their first product wasn’t Cursor. It was a Copilot for mechanical engineers. Their reasoning:

“We focused on the mechanical engineering space partly because it would be a niche space that was sleepy and uncompetitive.”

— Michael Truell (Co-Founder & CEO)

That bet didn’t work. The domain was too narrow, the feedback loops were too slow, and the real opportunity was sitting right in front of them in the tool they used every day.

The pivot happened when GPT-4 gave Truell a concrete glimpse of what was actually possible.

“The step-up in GPT-4 felt like, look, that really made concrete the theoretical gains that we had predicted before. It felt like you could build a lot more just immediately at that point in time. And if we were being consistent, it really felt like all of programming was going to flow through these models and it felt like that demanded a different type of programming environment.”

— Michael Truell (Co-Founder & CEO)

That phrase, all of programming was going to flow through these models, is the entire founding thesis of Cursor. Everything else follows from it.

Growth Lever 1: The fork that made no sense

When Cursor launched, every other AI coding company built a Copilot-style plugin for VS Code. Cursor forked the entire editor. At the time, this looked like a waste of months. VS Code had over 70% developer market share, the full backing of Microsoft, and a mature extension ecosystem. Rebuilding it meant reconstructing language servers, navigation, debugging, the integrated terminal.

The thought was around how models were getting better every month, but the Copilot experience hadn’t changed. “Why are these guys not making new things?” was the question driving the fork.

If programming itself was about to change, then a plugin wasn’t enough. Plugin extensibility is limited. When the paradigm is shifting under you, you need the entire application.

The bet paid out the moment AI-native UX started mattering more than incremental autocomplete. Chat-in-editor, agent panels, multi-file edits, Tab predicting your next several changes across files: all of these required editor-level control that no plugin architecture could deliver. Cursor’s UX surface became the moat.

“A lot of the things that we build and then we try them out, we do an experiment and then we actually throw them out because they are not fun. And so a big part of being fun is being fast a lot of the time. Fast is fun.”

— Arvid Lunnemark (Co-Founder)

Growth Lever 2: Build for monks, not the masses

Cursor explicitly rejected the democratization narrative.

Cursor had turned down the idea that the goal was to make coding accessible to everyone, and focused instead on the most demanding professional developers on earth.

“We kind of lived like monks in 2023 and just focused on the product. And it really just spread from word of mouth.”

— Michael Truell (Co-Founder & CEO)

The product development process matched the philosophy. The default at Cursor was biasing toward release the moment something showed signs of usefulness. Meaning, releasing half-finished things their competitors wouldn’t ship. The shipping cadence was the strategy.

The thing they were most careful to avoid was the trap called the siren song.

“One of the siren songs involved in building AI products is optimizing for the demo. We were really nervous about optimizing for the demo because with AI it is easy to take a couple of examples and put together a video where it looks like you have a revolutionary product. And then there is a lot of work between the version that can result in that great looking demo and then a useful AI product.”

— Michael Truell (Co-Founder & CEO)

The protection against the siren song: they were the users. All four founders used Cursor as their daily driver. They couldn’t ship something they didn’t want to use themselves.

ACT 2: The PLG machine

$4M to $300M ARR (April 2024 to April 2025)

Growth Lever 3: Tracking the metric “Paid Power Users”

Almost every growth-stage company tracks DAUs, MAUs, signups, and activation rates. Cursor tracked something different.

“We looked at revenue, we looked at paid power users — measured by, are you using the AI four or five days a week? Not DAUs, not MAUs. We’re a tool that serves professionals, and the real costs mean we care about you graduating to that paid tier.”

— Michael Truell (Co-Founder & CEO)

This metric choice had downstream consequences on every product decision. Features weren’t evaluated by whether they increased signups. Rather, they were evaluated by whether they made someone already using Cursor want to use it four or five days a week instead of three.

The freemium conversion mechanic followed from this. Cursor didn’t gate features behind a paywall. Power users hit usage limits naturally and upgraded themselves. By early 2025, Cursor had 360,000 paying users. The average spend was $276 per year. Sacra reported a 36% conversion rate from free to paid, roughly ten times the industry standard for freemium SaaS.

None of that happened by accident. It happened because the metric the team optimized for aligned perfectly with the business model. Paid power users are the only users whose behavior justifies the inference costs. When you track the right metric, the entire product strategy becomes coherent.

Growth Lever 4: $0 in marketing, and the power of word of mouth

Cursor grew to over $200M in ARR and over a million daily users without spending a dollar on traditional marketing.

“Some of the normal things that people would maybe reach for in building the company early on, we really let those fires burn for a long time, especially when it came to things like sales and marketing.”

— Michael Truell (Co-Founder & CEO)

What grew instead was entirely organic. Developers posted screenshots of things Cursor had done that no plugin could do. Vibe coding became a meme. An 8-year-old’s Cursor demo went viral. Voice-coding clips spread across developer X/Twitter. The team amplified user wins, leaned into the meme, never tried to control the narrative.

Cursor passed that test. The product was genuinely, obviously, radically better. And an order-of-magnitude better in specific moments developers could screenshot and share without needing to explain them.

Growth Lever 5: Logos before the sales motion

Cursor’s early customer list was built through bottom-up adoption, including customers like OpenAI, Midjourney, Shopify, and Instacart. Developers expensed it, IT teams noticed the spend, and enterprise conversations started because developers were already there.

The moment that signaled the shift from organic to institutional was Jensen Huang publicly calling Cursor his favorite enterprise AI service in late 2025. NVIDIA reportedly reached 100% engineer adoption. Salesforce had 20,000 engineers using it. More than half the Fortune 500 was in the customer base by June 2025.

The talent dynamic is like a flywheel for Cursor: nail the first ten hires, and the next person walking in is shocked by the density and excited to be there.

The same logic applies to enterprise logos. When the best developers at a company adopt a tool, their colleagues notice. When the whole engineering team is using it before procurement has been involved, the sales motion’s job is just to formalize what’s already happening.

By the time Cursor hired former Rubrik President and CRO Brian McCarthy as President of Global Revenue in February 2026, there was a $2B ARR business to formalize. The enterprise motion arrived after the demand.

ACT 3: The enterprise unlock and the data flywheel

$300M to $2B ARR (April 2025 to February 2026)

This is the act where multiple compounding forces hit simultaneously. The PLG flywheel was already spinning, enterprise customers were knocking, and Cursor made a product bet in private that changed the unit economics of the entire business.

Growth Lever 6: The enterprise pivot: done late, done right

The revenue composition shift at Cursor is one of the clearest illustrations of what PLG-led enterprise actually looks like in practice. At $400M ARR in late 2024, corporate buyers were roughly 25% of revenue. At $1B ARR in November 2025, enterprise had grown to about 45%. By $2B ARR in February 2026, enterprise was nearly 60%.

The mechanics of how that shift happened matter. Companies that had run three to six month pilots through mid-2025 began signing organization-wide deployments in Q4 2025, locking in 500 to 5,000-plus seats at $40 per month per developer on annual commitments. The sales motion never had to generate cold demand. It just had to show up and close.

The team stayed brutally lean through this growth. Most software companies hit 100+ headcount by the time they have 40 engineers, buried in operational work and sales-led from day one. Cursor started incredibly lean and product-led and stayed there.

At roughly $300M ARR, Cursor had 60 employees. That ratio of revenue per employee is almost without precedent in software history. It was only possible because the product was doing most of the enterprise sales work.

Growth Lever 7: The custom model bet

When Cursor started, they had no plans to train their own AI models. They were a product company using frontier models as infrastructure, the same way every other AI application company was operating.

Then the product surface forced their hand.

“We definitely did not expect to be doing any of our own model development when we started. In fact though, we do a ton of model development. At this point, every magic moment in Cursor involves a custom model in some way.”

— Michael Truell (Co-Founder & CEO)

The specific technical need: predicting the next several edits across files in 300 milliseconds at fractional cost. No frontier model could serve that use case well at scale. Cursor’s Tab feature, which anticipates and suggests entire code changes before a developer types them, required a model trained specifically on what developers accept, modify, and reject.

That data isn’t available to anyone else. Every line of code accepted or rejected inside Cursor is training signal that compounds. The Composer model launched in October 2025.

AI coding mirrors search at the end of the 90s. The product ceiling is high, distribution makes the product better, and the more people using it, the more you see where it falls over. The data flywheel and the product ceiling are coupled, owning one accelerates the other.

By April 2026, it was reported that Cursor had reached slight gross-margin profitability, driven in part by routing an increasing share of completions through its proprietary Composer model rather than paying Anthropic and OpenAI inference costs. The unit economics story is still early but the direction is clear.

The Founder Behind the Numbers: Interesting things Michael Truell believes

Michael has shared three beliefs sabout how he thinks what Cursor is building and where software development is goingP

On what survives AI taking over most of software

This is the question every developer is asking.

“We think that one thing that will be irreplaceable is taste. So just defining what do you actually want to build? People usually think about this when they are thinking about the visual aspects of software. I think there is a taste component to the non-visual aspects of software too about how the logic works.”

On the vision that started everything

Cursor’s company manifesto explains every product decision the company has made:

“We are an applied research lab building extraordinary productive human AI systems. To start, we are building the engineer of the future, a human AI programmer that is an order of magnitude more effective than any one engineer. This hybrid engineer will have effortless control over their codebase and no low entropy keystrokes. They will iterate at the speed of their judgment, even in the most complex systems.”

On why no moat is permanent

He is unusually candid about the limits of competitive advantage in a market where AI capabilities improve as fast as this one.

“I truly just think that the ceiling is so high that no matter what entrenchment you build, you can be leapfrogged. The sad truth for people like us, but the amazing truth for the world, is there are many leapfrogs that exist.”

— Michael Truell (Co-Founder & CEO)

Quick Reference: 7 growth levers at a glance

- The Fork: Own the surface when the UX paradigm is shifting. A plugin gives you a seat. An editor gives you the table.

- Build for Monks: Serve the most demanding users obsessively before trying to democratize. The mass market follows the power users.

- The Right Metric: Track paid power users who use the product four to five days a week. Everything else is vanity.

- Zero Marketing: A product creating wow moments in under five minutes of use doesn’t need acquisition spend. It needs retention.

- Logos Before Sales: In bottom-up DevTools, developers smuggle the product in. The enterprise motion formalizes what already exists.

- Enterprise Late, Done Right: Layer the sales motion on top of pre-qualified PLG demand. The order of operations is the strategy.

- The Data Flywheel: Proprietary usage data that improves the product is the only durable AI moat. Get in the critical path of professional workflows.

Tag @GTMnow so we can see your takeaways and help amplify them.

More for your eyeballs

Vanta crossed $300M ARR, just nine months from $200M to $300M, with acceleration each quarter.

Owner hit $1B in sales for local restaurants and just launched Grader, an AI CMO built for independents who can’t afford one. 60M+ users are already interacting with local restaurants through the platform.

Anthropics’ pre-IPO valuation has officially hit a record of 1 trillion. It has crossed the $1 trillion line, joining OpenAI and Space X as the third private company to hit that mark. This is an implied valuation coming from secondary market trading.

More for your eardrums

GTM 188: What Flipped Okta from $850M in Losses to $760M Profit | Jon Addison

VC: Inside a16z’s $1.7B Infrastructure Bet | Jennifer Li, General Partner

Listen through the links in the page above or by searching wherever you get your podcasts “The GTMnow Podcast.”

Startups to watch

Hightouch – raised $150M at a $2.75B valuation to build the agentic marketing platform: AI agents that run on your actual customer data to research audiences, generate creative, and execute campaigns 24/7.

Monk – just raised a $25M Series A (Footwork + Acrew Capital) to fix B2B collections, the $3T sitting in U.S. accounts receivable that takes 45-90 days to actually land.

Hottest GTM jobs of the week

- Head of Marketing at BlueCargo (New York, NY)

- Mid-Market Account Executive at CaptivateIQ (Hybrid – Austin, TX)

- Product Marketing Manager at Esper (Hybrid – Austin, TX)

- Growth Marketer at Tavus (San Francisco, CA)

- Head of AI & Revenue Operations at Noibu (Hybrid – Ottawa, Canada)

- Enterprise Account Executive, US & Canada at Semrush (Dallas, TX)

See more top GTM jobs on the GTMfund Job Board

GTM industry events

Upcoming events you won’t want to miss:

- SaaStr Annual: May 12–14, 2026 (San Mateo, CA)

- GTMfund Dinner: May 14, 2026 (San Francisco, CA)

- RevStar Summit: June 3, 2026 (Toronto, Canada)

- GTMfund Dinner: June 9, 2026 (London, UK)

- Dreamforce 2026: September 15–17, 2026 (San Francisco, CA)

- INBOUND: September 16–18, 2026 (Boston, MA)

- Pavilion GTM2026: September 28–October 1, 2026 (NYC, NY)

- CVC Week by Counterpart Ventures: September 29, 2026 (San Francisco, CA)

- Customer Success Week: October 5-9, 2026 (NYC, NY)

- TechCrunch DISRUPT: October 13–15, 2026 (San Francisco, CA)

GTMnow community love

Some GTMnow Network love to close it out – we appreciate you.